Many pundits have talked about “the Fourth Industrial Revolution,” but what does it mean? Franklin Equity Group’s Matt Moberg explains in the below podcast how the current pace of innovation is driving productivity gains—and accelerating economic growth.

Podcast: Investment Opportunities Resulting from Accelerated Disruption – link here

Innovation has persisted throughout the course of history, but it has not always progressed in a predictable or linear fashion. Innovation is episodic. Periods when we have seen increases in new ideas and technologies typically coincide with sustained and accelerating economic growth.

Consider: Growth in the Western world from AD 1 to AD 1820 was approximately 6% per century. By comparison, Americans enjoyed a doubling of real output every 32 years throughout the 20th century. Before then, real output required 12 centuries to double.

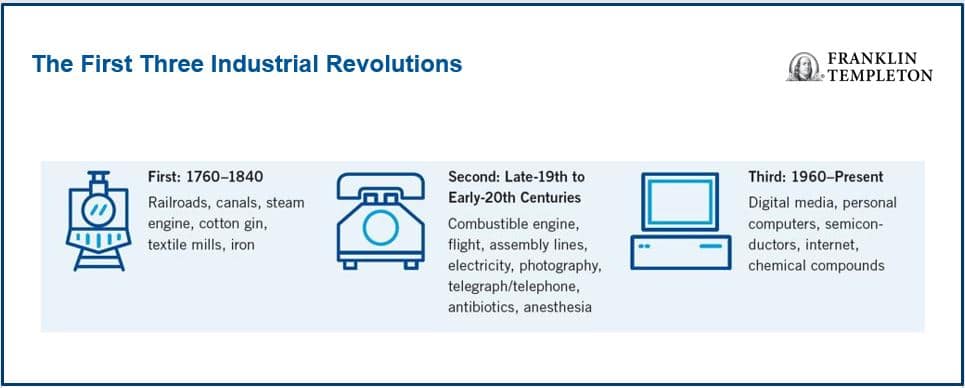

Economists define these periods as industrial revolutions. Typical of their creativity, they refer to them as the First, Second, Third and Fourth, the First beginning in 1760.

We believe we are living through the Fourth Industrial Revolution today, and that it is driving the current pace of innovation in the marketplace. Building on the Third, a digital revolution occurring since the mid-20th century, the Fourth reflects many technologies—blurring the lines between physical, digital and biological spheres.

Increased Productivity Increases Wealth Creation

As investors in innovation, the transformational impact of the Fourth Industrial Revolution supports the five platforms of growth we have previously discussed. Technological and industrial advancements increase economic productivity, which is foundational to wealth creation. Paul Krugman, Nobel Prize winner in economics, noted: “Productivity isn’t everything, but in the long run it is almost everything, as a country’s ability to improve its standard of living over time depends almost entirely on its ability to raise its output per worker.” Today, the average American only needs to work 11 hours per week to match the productivity of a 40-hour work week in the 1950s.

Real-World Examples of Increased Productivity

When I started my career, I was a bank auditor. In a bank, only the most senior members approved loans. It was typically done in group settings, with highly paid individuals sitting in conference rooms, reviewing files, crunching numbers and deliberating for hours. Today, with FICO (individual credit) scores, virtually no human being looks at any credit request below US$50,000. A computer does it all.5

In the days depicted in the popular TV show Mad Men, which took place in the 1960s and 1970s, advertising was sold based on the number of pages in a magazine or sold as a 30-second television slot. Sales were high touch and it was understood that much of advertising spending was “wasted.” In the current US$600 billion annual advertising market, Google, Facebook and others use algorithms to not only maximize revenue, but to also maximize return on investment (ROI) for their customers. Today, internet ad buying is not only the most automated advertising medium, it’s also the most effective. It can be effective as a branding or a direct-response event.

One of the most important aspects of any business is the pricing of products. Pricing is usually done with sales, finance and senior management working together to maximize profit. Historically, it was a very labor-intensive research exercise. Today, the pricing of enormous markets is entirely automated. Airlines, e-commerce companies and hotels, just to name a few, allow machines to price their offerings.6 These are some of the biggest revenue pools in our economy, all completely automated. Pricing can change based on real-time inventory availability, minute-to-minute demand, and even the weather. Algorithms attempt to maximize elasticity of demand across hundreds of thousands of products in real time.

This trend toward increasing productivity, a result of the Fourth Industrial Revolution, is only beginning, in our view. Over the next decade, we believe we will see major technology-driven efficiencies or product improvements in many areas. These will include insurance, medical diagnosis, automotive distribution, industrial design, the pricing and exchange of capital, and the analysis of data.